April continued the March boom, with the US leading the way, buoyed by a swift vaccine roll-out and fiscal stimulus measures. Investor sentiment was supported by the combined economic and policy backdrops, but also a robust US earnings season.

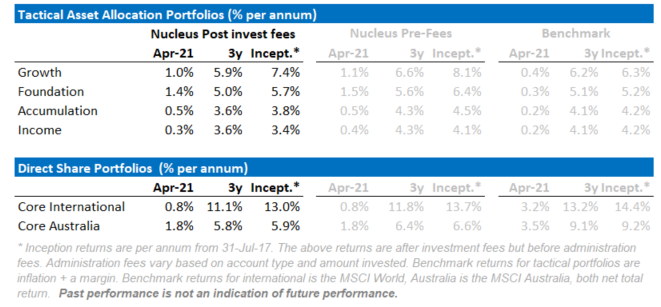

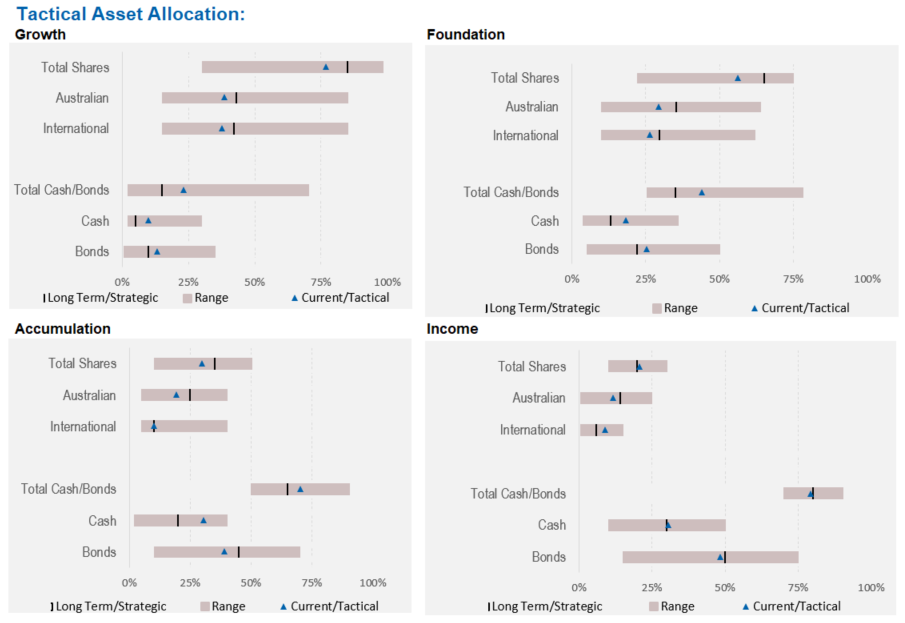

Our asset allocation portfolios all posted positive returns for the month, and continue to deliver significantly lower volatility than the market.

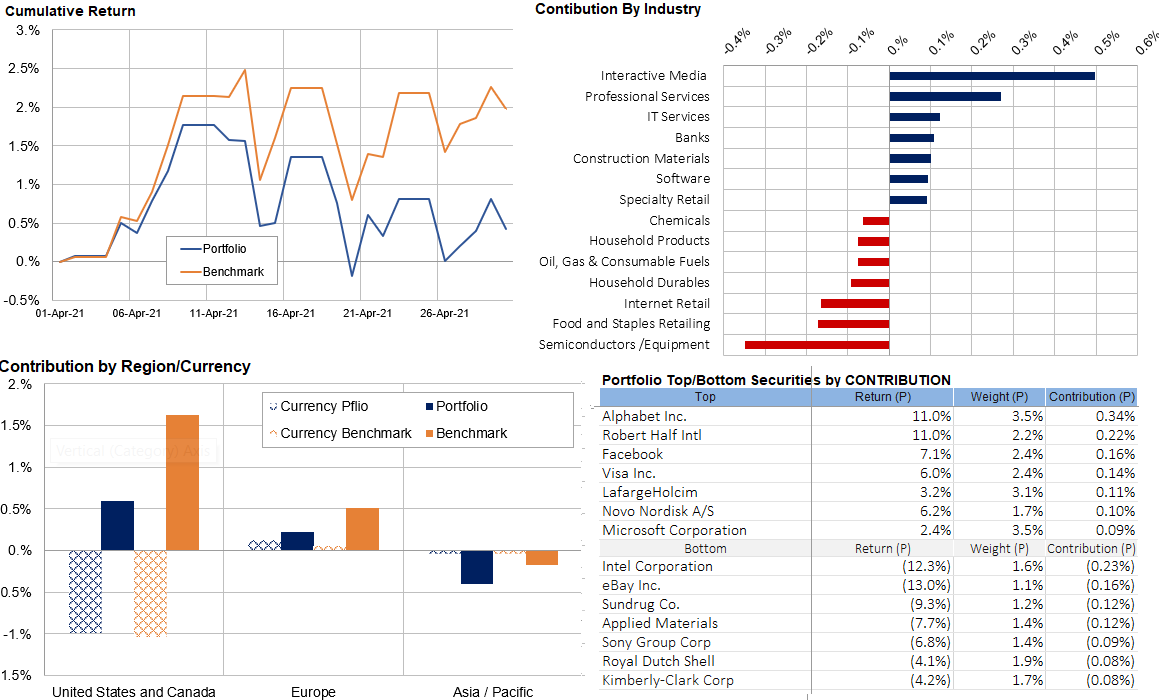

More importantly, it was a reversal month. Value stocks performed strongly in March (and again so far in May) - and our portfolios are leveraged to that trade. The reversal in April meant that we did not rise as quickly as the market, but our underperformance has been erased so far in May as markets returned to the value trade.

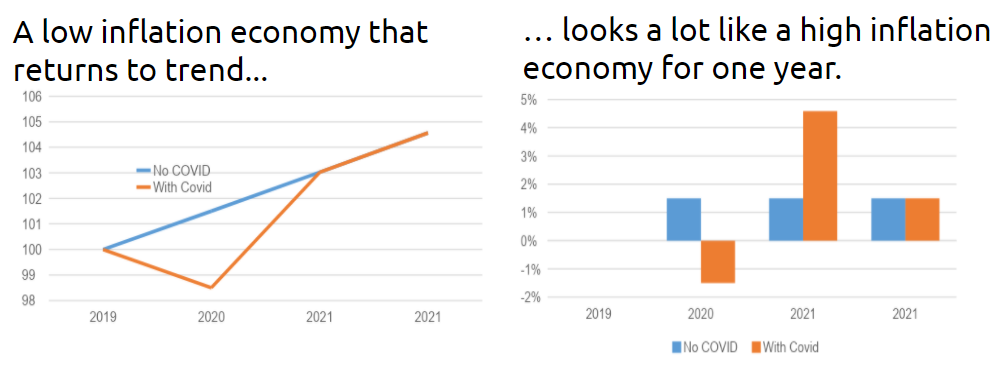

We have been warning for months that markets will get carried away with extrapolating short term inflation long into the future. This month we saw high inflation prints in the US and we expect inflation will stay high in the coming months. But most of the inflation is either in the supply chain or comes from low base effects, both of which will pass.

Inflation is not well understood. Most central banks have been trying to create inflation for the last decade. And failing. The Bank of Japan? 30 years.

In 2010, many prominent economists were so sure hyperinflation was coming that they wrote an open warning to the then head of the US Federal Reserve. No inflation.

This isn't to say we know nothing about inflation. But it does mean that we need to approach inflation forecasts with skepticism and keep an open mind on outcomes.

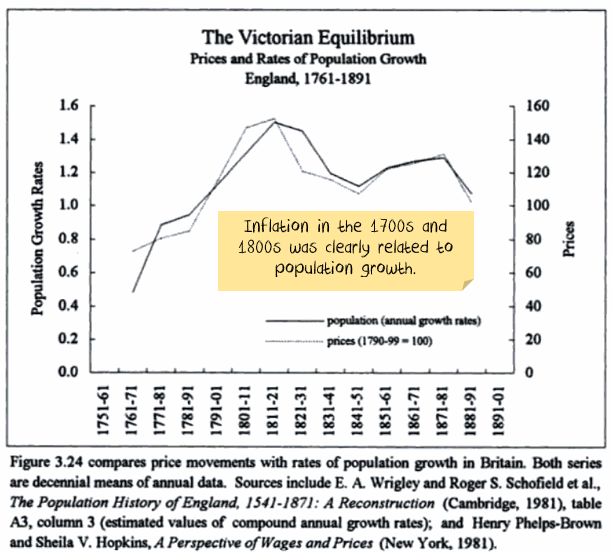

Pre-1900, inflationary bouts were common. They tended to coincide with either population growth, famines, war or monetary debasement.

Today's economies are different. The factors that cause inflation in agricultural societies are not the same as in a modern economy.

Population growth will still affect inflation, but population growth is very low relative to historical levels.

The world struggled with both high inflation and high unemployment for most of the 1970s and 1980s. This is the scenario that technocrats are looking to avoid.

It is worth noting three other important factors:

Inflation expectations became entrenched. Employees demanded continual wage rises to offset the effect of the higher expected inflation.

Companies had to raise prices to keep profitable. Meaning employees needed a pay raise. Rinse. Repeat.

Stagflation was cured in the 1980s. The narrative is inflation was solved by the US central bank, which raised interest rates high enough to stamp inflation out. i.e. the central bank was prepared to cause a recession to "anchor" inflation expectations.

Just as importantly, new rules were enacted to "ensure" inflation wouldn't return:

Arguably, the pendulum has swung too far. The steps taken to prevent inflation have entrenched disinflation.

Low inflation expectations became entrenched. Employees stopped demanding continual wage rises. Unionisation rates plummeted.

Additionally, China entered the World Trade Organisation and started routinely exporting deflation in the form of lower prices for manufactured goods.

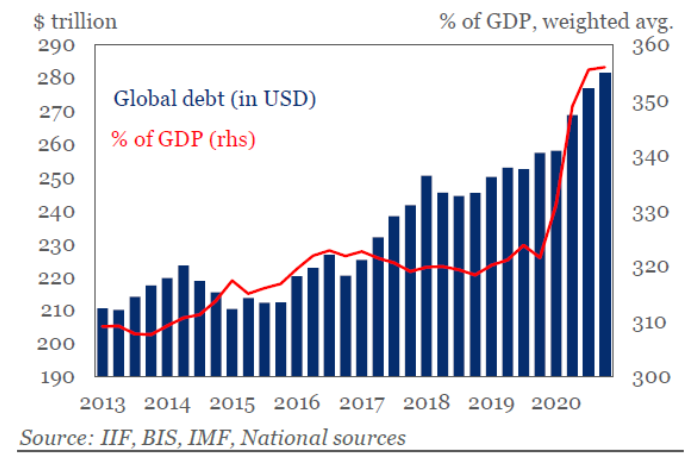

Debt is a two-edged sword when it comes to inflation. Increasing private debt levels can drive inflation higher while the debt is accumulating.

However, unless private incomes also increase, high debt levels serve to decrease demand.

i.e. if the debt is created for productive assets like buying new businesses or infrastructure, it can quickly pay for itself.

Suppose the debt has been accumulated in non-productive assets like bidding house prices higher. In that case, there is more likelihood that it will slow inflation.

Debt levels are high. Wage growth is low.

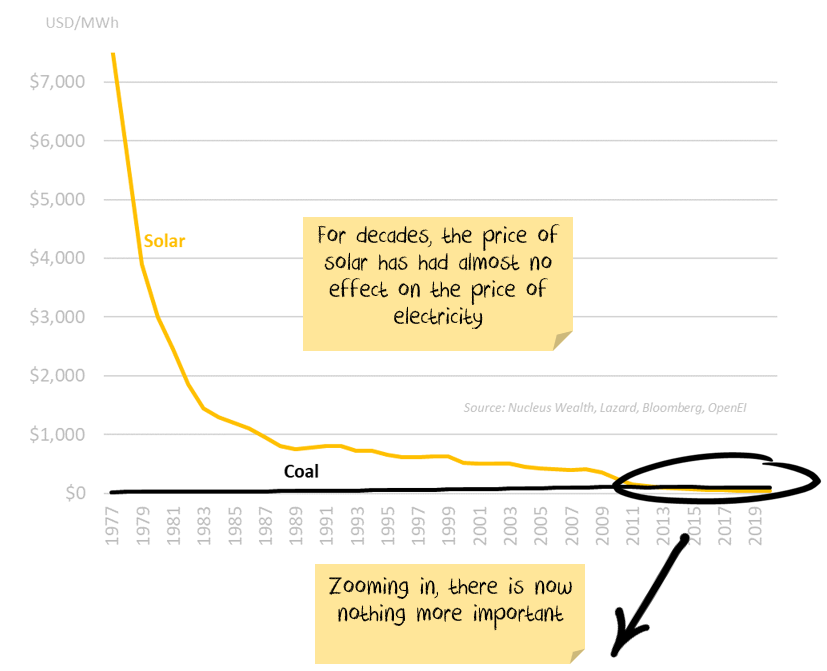

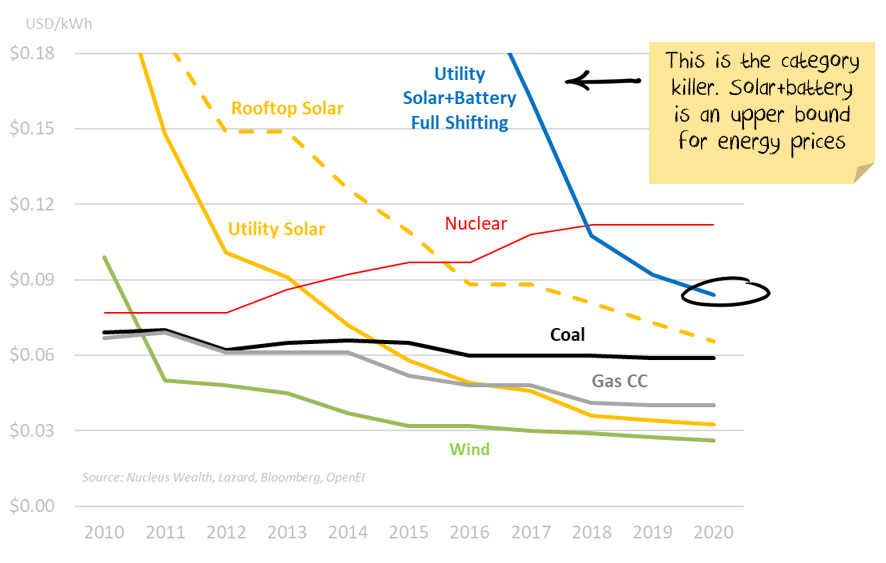

Technology is inherently deflationary. Incremental improvements are at the heart of capitalism. In recent decades the internet disintermediated entire industries, reducing costs, increasing competition and lowering inflation.

In the next few decades, power grids will either evolve or collapse. The age of centralised energy is all but over. Ahead lies a radical evolution to the decentralised and local. Moreover, as it is completed, energy costs will continue to decline every year, sourced from sun and wind every day and stored in little boxes of chemicals.

The productivity and income gains implicit in this are immense. Every bit as large as the steam and oil revolutions before it.

Any and every repetitive function in the economy is going to be inhabited by a robot. Everything from manufacturing to driving is in the cross-hairs.

Technological advancement will destroy jobs. But the productivity gains that come with it will lift incomes for both capital and labour. This will create demand and investment in new and more efficient segments.

There will be a major question about the disruption of job losses. Done well, part of the productivity gains will be temporarily used to transition those who have lost jobs into the new economy. Done poorly, soaring unemployment will create political chaos.

Either way, the forces are deflationary.

Inflation is too much money chasing too little goods or services. Short term issues like weather or supply chain bottlenecks do not create lasting inflation.

What can create lasting inflation?

Just as importantly, in the 1970s and 1980s, weak consumer demand was not an issue. In the 2020s, it is. Higher oil prices act as an additional tax on consumers.

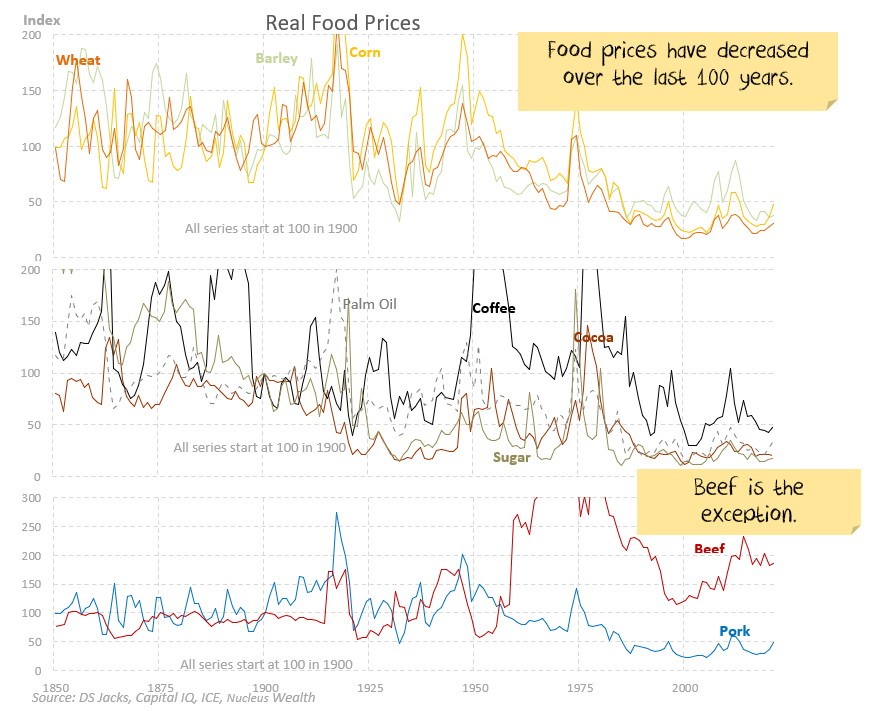

Can there be a short term spike in food prices? Yes, but in developed countries, food is a low of overall prices. And much of the cost of food is in the preparation costs, which is about wage inflation.

Inflation is not a "one-period" issue. For inflation to persist, the supply issues will need to be maintained. And maybe even get worse every year. This is not a likely outcome.

The worst scenario for inflation?

We have taken a nuanced investment strategy for the last few months. We don't believe the inflation will be real. But we do believe the market will treat the inflation as real.

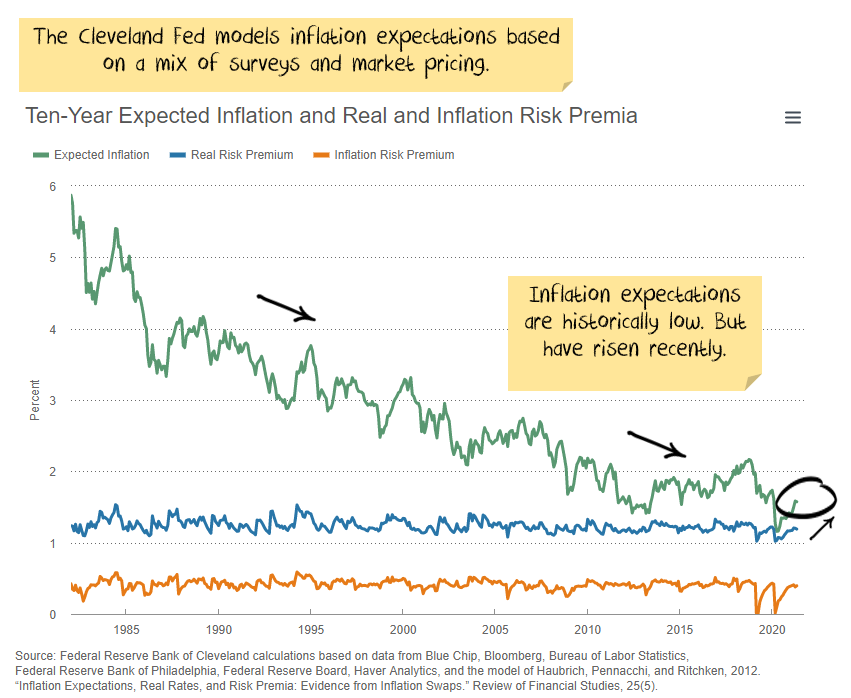

As we predicted, it is easy for the market to believe rates are on hold forever when inflation is 1%. It is another thing when inflation prints 4%. Even if the 4% is a temporary number.

The inflation mirage has not finished. There are at least a few more months before inflation will fall. And the inflationistas are out in force.

This means the trick is maintaining enough inflation protection to hedge against continued inflation concerns, while we wait for the right time to take the opposite stance. The benefit is that if signs emerge that inflation will continue then there will be little lost in reversing course.

As the switch into value continues, the key for us is maintaining protection. Markets continue to be expensive and while the grind higher is likely, there are also considerable downside risks.

The equity market continued to climb over April, building on the March gains. Our Core portfolios produced gains but underperformed their respective indices, as some of our value plays took a breather, and growth stocks posted strong gains. We refrained from any major stock changes this month.

Our international portfolio saw a 0.8% increase over April. Some disappointing earnings results from Ebay and Intel were offset by a strong performance of Internet stocks. The currency effect was the opposite of March detracting from US returns but helping European performance.

The Core Australian portfolio underperformed the index this month as travel stocks faltered and our new USD earners suffered due to the currency headwinds.

Damien Klassen is Head of Investments at Nucleus Wealth.

Follow @DamienKlassen on Twitter or Linked In

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen is an authorised representative of Nucleus Wealth Management, a Corporate Authorised Representative of Nucleus Advice Pty Ltd - AFSL 515796.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}