With decent investment yields increasingly hard to find, it is important to avoid yield traps when looking for alternatives to increasingly expensive bonds.

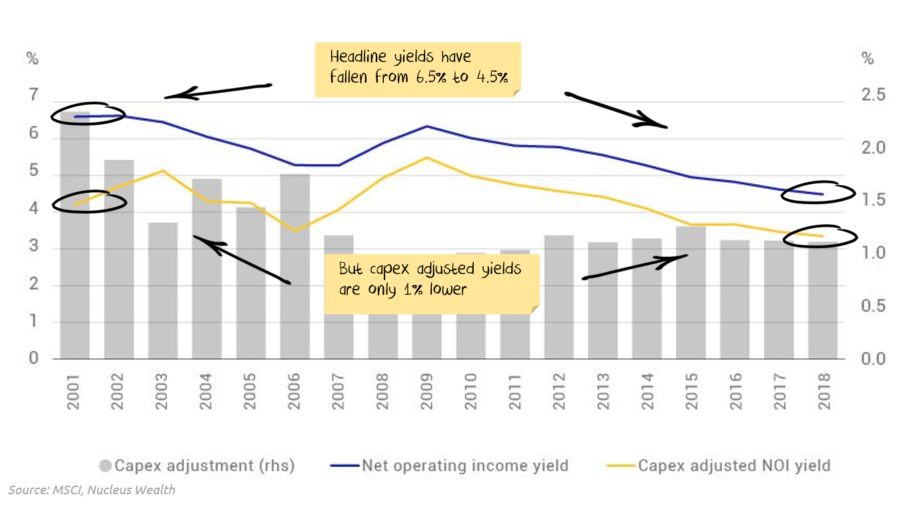

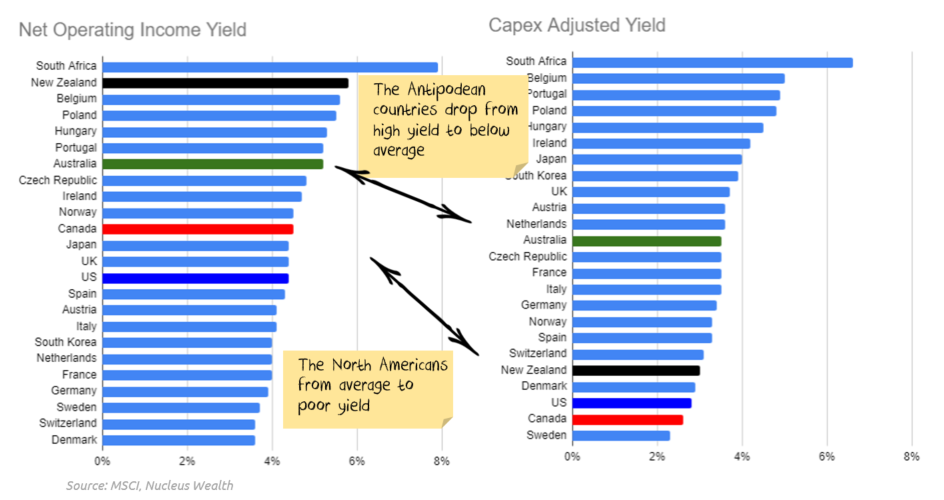

Looking beyond the headline yield is critical to avoid the pitfalls: sustainability of yield, adjusting for capital expenditure, incorporating buybacks and analysing cyclicality of earnings can all help. MSCI came out with a useful reminder last week of the dangers of relying too much on headline yields for listed real estate companies, but MSCI buried the lead. Key issue: High headline yields don't always mean high returns after adjusting for capital expenditure.

Secondary issue: yields adjusted for capital expenditure (capex) haven't fallen as far as the headline yields. At yields of 3.5% vs negative yields across European government bonds, we have the perverse situation where investors are buying bonds for capital appreciation and stocks for yield rather than the other way around.