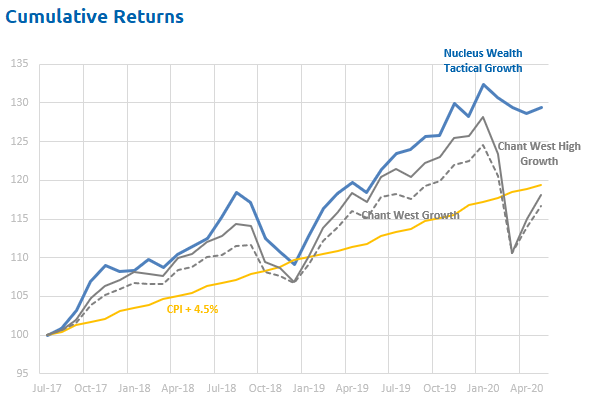

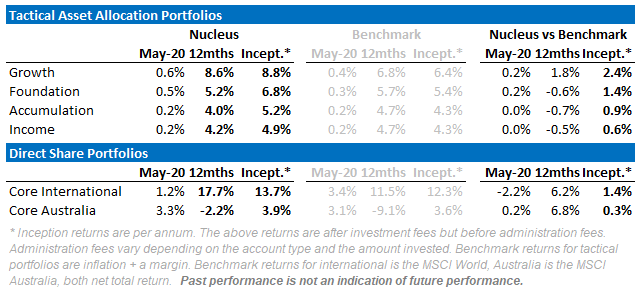

May saw share markets extend their bounce in the face of worsening economic conditions. In particular the last week of May and the first week of June we would characterise as a blow-off top. Value and cyclical stocks rallied hard, completely at odds with earnings and economic outcomes. Our portfolios continue to be positioned for further downside and so only took a limited part in the bounce. Over the last year, our Tactical Growth fund is beating the Chant West median high growth superannuation fund by 8%. In our direct equity portfolios, we have long preached the idea of holding a mix of quality and value to provide downside protection - and that showed this year. Our International fund is beating the MSCI World by 6.2%, our Australian fund is beating the MSCI Australia index by 6.8%.

Stock markets are almost as expensive as they have ever been on a range of different measures. The economy is almost as bad as it has ever been on a range of different measures. Take note of the analysts who are contorting themselves trying to reconcile the two and telling you to keep buying. These are probably the same analysts who cheerled the stock market at the peak of the Dot-Com bubble or just before the financial crisis.

Last week I wrote You are being given a rare second chance to sell stocks. This week I'm interested in how much further the Virus Bubble can run before collapsing.

Is the Virus Bubble going to run for years like the tech boom, or is it more like the 2015 China stock market boom and over in a matter of months?

First, it's important to know what type of bubble we are dealing with - it is not a typical one. I'm going to look at the current bubble through the lens of James Montier's four flavours for some context:

Given the Virus Bubble is a mix of an Intrinsic and an Informational bubble, it gives us clues as to what the demise will be.

Informational bubbles end when other investors start selling, and everyone stampedes for the exit. So, that is no help on timing.

Intrinsic bubbles end once the irrationality of the earnings is acknowledged. My best guess is a mix of bankruptcies and continued weak earnings will eventually do it. It might take six months. It might take six minutes.

A Biden win in the US election, or even the increased threat of one, has the potential to shock the market into a dose of reality with the spectre of higher taxes and wages eating into profits.

In the meantime, the question is how much bigger can the bubble get?

Bubbles rely on new money to keep them inflated or growing. So, as long as new money is flowing, the stock market bubble can keep growing.

This bubble does have a higher hurdle. Many bubbles come with increased profits which are reinvested and help to sustain the bubble. The Virus Bubble is the opposite, it needs new money just to fill the hole that reduced earnings and increased debt are leaving behind. Only after that can it grow.

There are four primary sources bubbles rely on for new money:

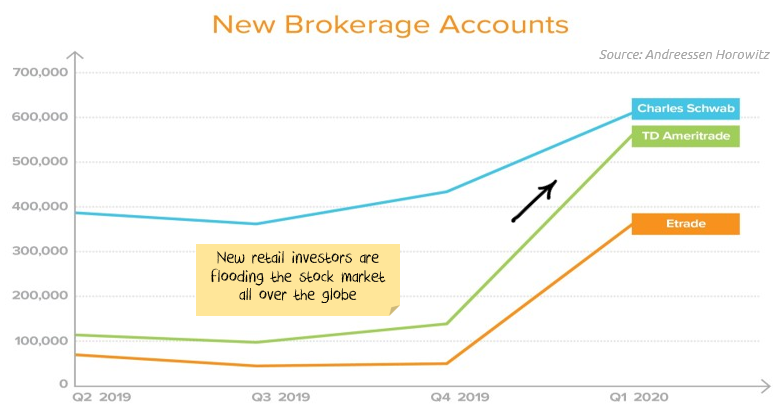

Globally there has been a rush of new, generally younger investors into the market:

The numbers sound impressive. Robinhood, a popular new US trading platform, has added 3m accounts this year. If you take the top 4 US online brokers, we can find another 3m accounts in the first quarter alone. Australia, at less than a tenth of the size of the US, in a six week period added 280k new and reactivated accounts. UK firms are reporting up to 300% more new accounts in the first three months. It is a global phenomenon.

But these numbers need context. The tech boom in 2000 was also (in part) driven by new retail accounts, peaking at around 19m US households with at least one trading account (noting a different definition of accounts) in 2001. That fell to 17m a few years later where it has remained since.

If we assume 9m new US accounts this year, and 65% already had a household account = 3m new households with accounts. That would put household accounts above the Dot-com boom peak.

Two conclusions: (a) the numbers are significant (b) we have probably seen most of the increase in accounts already.

One more potential thought: Has the increase been bored workers stuck at home? If so, with sport resuming in Europe and Australia, it will be interesting to see if retail trading drops away in those locations.

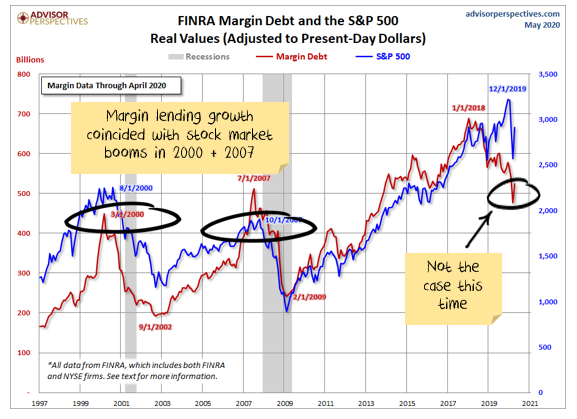

Many booms involve a significant increase in debt to fuel asset price growth. Given the speed of the market rise, and the number of new accounts, it seems unlikely increased gearing has played a meaningful role in the boom.

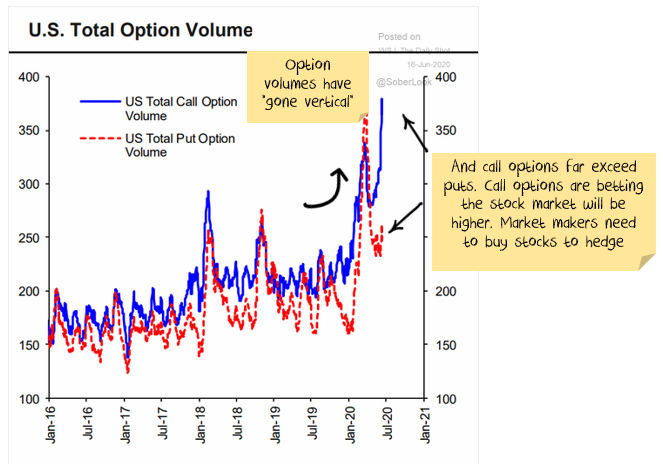

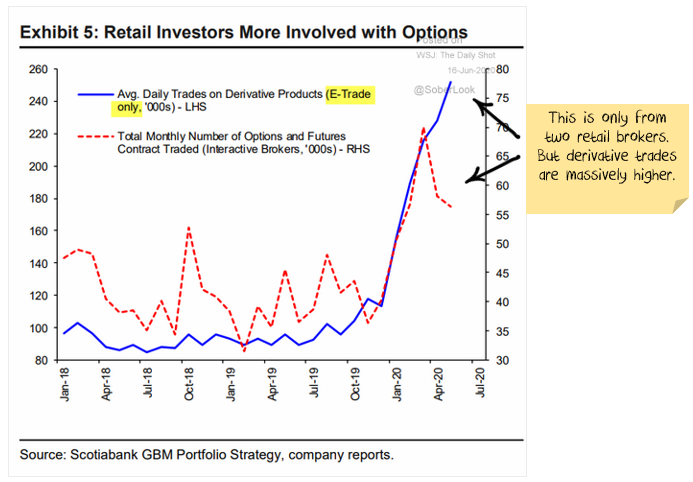

Gearing doesn't just have to be through debt. The other way to get leverage is through derivatives which can increase the return (and the risk) by many multiples of the investment.

While the investor themselves might not be buying the stock, the market makers who are selling the derivatives need to purchase the shares to hedge against losses.

There has been a lot of increased derivative trading.

The final way to get more money into a stock market bubble is to transfer money from other asset classes. This comes in two parts:

Central banks are encouraging stock investment. By buying government debt, they are hoping to force investors to shuffle up the risk spectrum.

Having said that, governments are also issuing massive amounts of debt.

So, to get investors to switch into equities, central banks need to buy more debt than what governments are issuing - otherwise the opposite will happen.

In context, the US government had about $23 trillion of debt at the start of the year, $25 trillion at the beginning of May.

Over the same timeframe, the US Federal Reserve assets rose from $4 trillion to $7 trillion. US debt will probably increase by about another $4 trillion in 2020. So, if the US Federal Reserve does not also increase its balance sheet by $4 trillion, then money will flow into government bonds from other assets.

Also, corporate debt is rising on the back of lost sales. So, going forward, the Fed will need to increase its balance sheet enough to cover all of the government debt and all of the new corporate debt.

Then, repeat this problem in just about every country globally.

Otherwise, money won't keep flowing into the stock market.

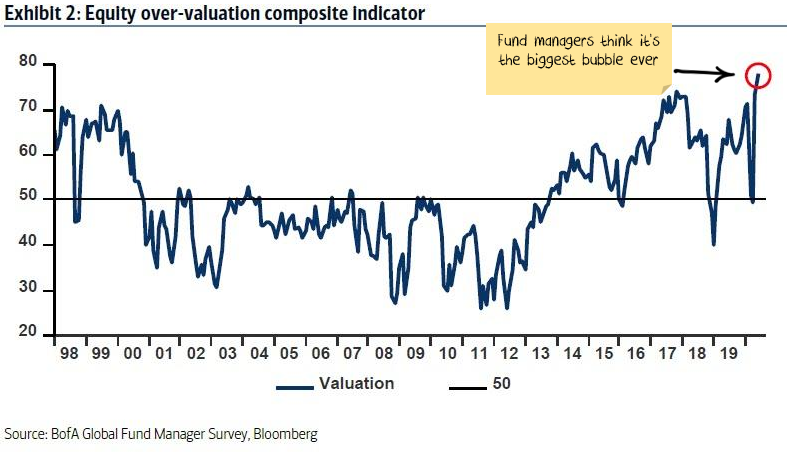

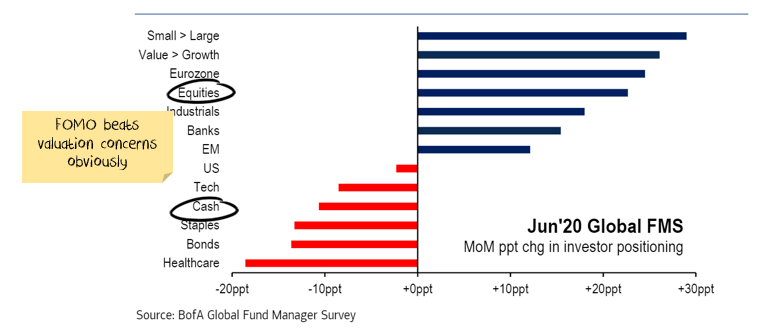

According to the latest Bank of America survey, fund managers agree that the stock market is overvalued:

And in April (reported in May) they acted that way:

But not in May. Fear Of Missing Out (FOMO) took over, and they were buying stocks:

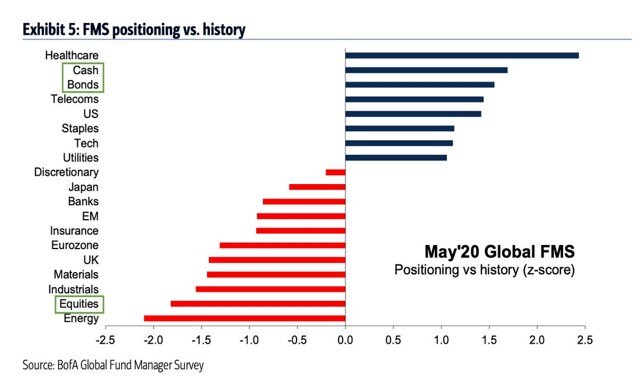

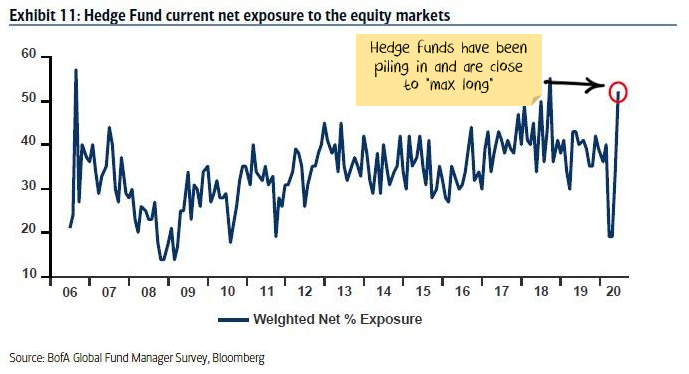

And hedge funds now have one of their highest ever weighting to the stock market - which suggests they are unlikely to buy much more.

Keep in mind that all bubbles are built on a grain of truth. That truth here is that central banks and governments "have your back" and will buy anything and everything to keep the stock market high.

I think central banks will continue to bail out corporate debt markets where they can. But already we are seeing cracks with Hertz and several airlines filing for bankruptcy.

The more significant issue is small and medium businesses which (a) make up 50-70% of most economies (b) don't have traded debt that central banks can buy.

The closest analogy to the current one is probably the 2015 Chinese stock bubble. The Shanghai composite index rose over 60% from February to June 2015. It then crashed back to prior levels over the next three months.

The growth was driven by a similar (15-20%) increase in retail trading accounts as we have seen in the US. The narrative was faith in the government and central bank. The end was weak economic data. The differences are: there was far more margin lending in the China stock bubble, but greater use of derivatives in the Virus Bubble.

Where does that leave us?

The US tech boom took about two years to play out, but was a different type of bubble. The China 2015 Bubble took four months before economic reality sunk in.

I expect the Virus bubble will be closer in timeframe to the China bubble than to the Dot-Com Bubble. But bubbles often last longer than seems reasonable.

It has been a surprisingly raucous party in share markets but the hour is late, and the party seems to be dying down. Some partygoers are trying to find more alcohol to try to keep the share market party going. They may be successful. Regardless of their success in extending the party, given the amount of alcohol already consumed, you will feel a lot better in the morning if you leave the party now.

Our portfolios "went to ground" before the crisis hit, selling stocks and investing in bonds/cash/international currencies. All of our funds have a low weight to shares. This is a significant deviation and one that we have not undertaken lightly.

There is little to glean from how far GDP or earnings fall, or how far unemployment rises. The numbers are going to drop a lot and will eventually bounce back.

The focus for investors should be on where earnings can get back to over the next few years. And I'm struggling to find anyone with a credible earnings scenario that would justify paying current prices.

The best bullish argument? Capitalism is dead, therefore buy equities.

I don't think central banks and governments are planning on suspending capitalism. So for me, loading up on equities at close to record valuations going into an immense economic unknown is not the right play.

The stock market has already priced a V-Shaped recovery. Which means if there is a V-Shaped recovery, there is limited upside. But if there isn't a V-Shaped recovery, then there is a lot of downside.

Damien Klassen is Head of Investments at Nucleus Wealth.

Follow @DamienKlassen on Twitter or Linked In

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen is an authorised representative of Nucleus Wealth Management, a Corporate Authorised Representative of Nucleus Advice Pty Ltd - AFSL 515796.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}