One of our core investment themes is that international stocks are the best asset class for Australian investors at this point in the cycle. To date, this has been the right call, with our international portfolio increasing over 13% over the last 4 months on the back of a weak Australian dollar, favourable stock selection and strong international markets.

Last month we posed the question of whether its time to switch to a different asset class. In November we changed our answer to that question. While we think there is still significant scope for the Australian dollar to fall, we need to balance this with valuations and potential risks. To this end, we took some profits in a number of portfolios and increased our cash weights.

It’s a nuanced argument – balancing potential upside vs the risks. We have taken the view that we would prefer to see stock markets lower or a period of consolidation to allow fundamentals to catch up with prices.

To be clear, we don’t think that we have reached the end of the current investment cycle, especially so as the long-awaited Trump tax cuts are on the verge of triggering a late-cycle US boom.

Our suggestion continues to be that investors need to position their investments early rather than trying to time the market.

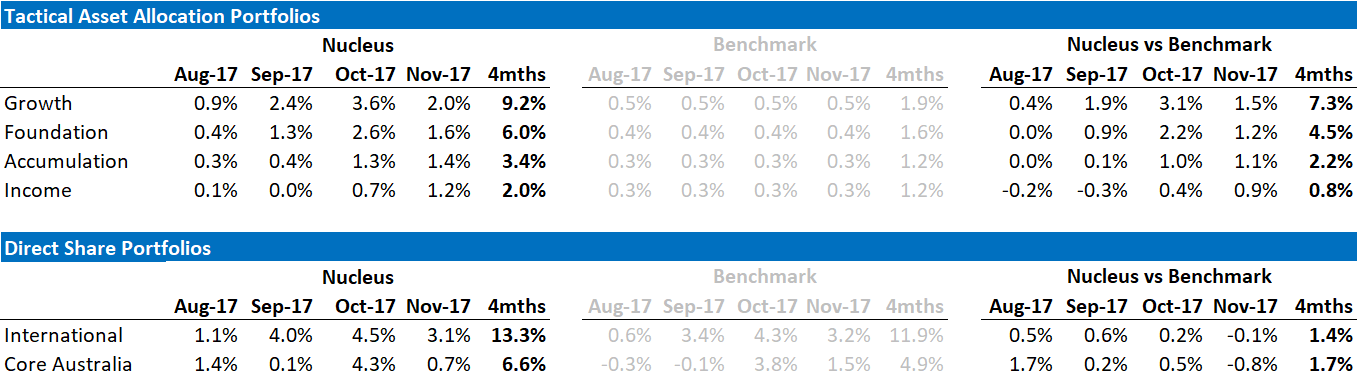

During November our Tactical Funds in particular continued to handily beat benchmarks:

The returns above include fees and trading costs on a $500,000 portfolio. Note that individual client performance will vary based on the amount invested, ethical overlays and the date of purchase. The benchmark returns do not include fees.

As a reminder, we look at the key themes facing our portfolios as being:

Trump tax cuts are now taking shape and there look to be relatively few impediments at this stage.

Our core position is that Trump is trying to engineer a boom. It will not be sustainable and will likely be followed by a bust that leaves the US economy in a worse position but that is a future problem – positioning the portfolio for the boom is the current issue.

The proposed tax cuts are badly targeted by giving most of the benefit to the rich and to companies, trickle down is unlikely to work, the tax cuts are unsustainable, and they are only a short-term “sugar hit” for the US economy, I understand all the negatives. But if it is anywhere near Trump’s promise then it’s going to be such a huge stimulus that you don’t want to stand in the way of it as an investor.

So, we want to play the boom, keeping a sharp eye on the bust. Valuations and sentiment have run so hard recently that we have pulled back our equity exposure. If we see earnings catch up or if we see a decline in markets, we will likely buy more equities.

Our portfolio positioning on this basis remains:

In China data continues to be muddied by winter/pollution shutdowns. Our view is:

Our expectation is that China is going to continue to “glide” lower to try to normalize the capital expenditure to consumption in-balance that we discussed in our recent webinar.

It is our view that the Chinese economy will continue to slow over the coming years – Japanese style lost decades, and low inflation/deflation remain more likely than a dramatic bust, which means a grind lower for commodities and the Australian dollar.

Our portfolio positioning on this basis remains:

In our tactical portfolios, we own cash, bonds, international shares and Australian shares. We tend to blend these portfolios for clients so that each investor receives an exposure tailored to their own risk and income requirements.

The broad sweep of our asset allocation over the last 12 months was to ride the Trump Boom, switch into Europe in March / April as the US became overvalued and then switch back into the US as the Euro rallied and the USD fell.

The next chapter, which we started during November, has been to reduce our international holdings after an almost 15% rise in the last 4 months.

Over the month our bond holdings added to performance, as expectations for interest rate rises in Australia were tempered. We expect this will continue to be a feature of the bond market.

We remain underweight shares in aggregate, slightly overweight international equities and significantly underweight Australian.

Our tactical foundation portfolio is designed for investors with lower balances, it uses exchange-traded funds for its international exposure rather than direct shares. The reason for this is parcel sizes, you can’t buy half a Google (Alphabet) share directly and so we use exchange-traded funds which buy baskets of stocks instead. The tactical portfolio is a balanced fund, not as aggressive in its holdings as the growth fund nor as conservative as our income fund.

Over the month in the tactical foundation portfolio, we sold down our international exposure from overweight to neutral. The fund continues to be underweight Australian stocks.

The key outperformer for the month was Footlocker in the US. Footlocker fell by 30%+ in the months after we purchased it due to fears of online competition. After much soul-searching on the viability of the business going forward, we decided to increase our weight and the stock jumped almost 50% over November. Other big performers for the month included Michael Kors (+25%), Southwest Airlines (+20%), United Therapeutics (+18%) and Robert Half (+17%).

At the other end of the spectrum Vestas Wind (-26%) continues to be plagued by concerns about the Trump administration pulling subsidies for wind power. We continue to treat this as a medium-term buying opportunity, acknowledging that sentiment will likely be poor for this stock for some time. Two of the car companies, Peugeot (-13%) and Linamar (-12%), gave back most of the prior months’ gains.

Defensives are expensive and so as we are letting go of some of our higher growth holdings, we are generally avoiding the traditional defensive sectors like REITs, Utilities, Telcos and Infrastructure. Our view is that (just as the central banks intend) lower risk investors continue to “shuffle up the risk spectrum”, and they have bid the price of traditional defensive sectors to levels that make investment difficult.

We are looking for a mix of the more stable industrial, consumer staples and healthcare stocks to get a similar defensive exposure without having to pay the nosebleed prices in the traditional defensive portfolios.

We have been overweight a range of automotive stocks and suppliers but have been winding the holdings back following a stellar share price run in the sector. The purchases were largely a value play as most of the sector trades on low multiples over growth concerns.

Our biggest call is underweight energy. In particular oil producers. We have blogged a lot about the oil price, the thumbnail sketch of the sector is that:

Meanwhile, oil stocks are pricing $60-$70 oil prices in perpetuity. The mid-term is going to have to be spectacular to justify current share prices, let alone getting any share price growth.

Having said that, it is a big risk to our portfolio being underweight energy. If there are geo-political ructions, particularly in the Middle East, we would probably underperform. October saw the oil price rise once more, largely on the back of hurricane-related supply constraints, but we remain comfortable with our holding and expect much of this to be a short-term issue.

Our sole holding in the energy sector, Neste Energy added 10% in November after 30% in October, which made up for any potential underperformance from being underweight with a rising oil price. Neste is a Finnish oil refiner, and at its interim results during the month provided an upbeat assessment of its future prospects leading to a range of analyst upgrades. Additionally, Neste is making a significant investment in green technologies and is well regarded by a number of sustainable rating firms including being in the Global 100 most sustainable companies, the Dow Jones Sustainability index and CDP.

We are underweight financials – mainly as we can’t find US financials that are cheap enough to justify purchasing. We have been trawling the European banks for value. Insurance continues to be a sore spot, there was some bounce back in insurance company share prices in October after a hurricane-affected September, but that reversed again for November. We are looking to continue to build holdings in the sector with the view that after such severe losses in 2017 that insurance premiums will rise significantly.

We have a reasonable tech / IT exposure. There are a number of smaller tech stocks that we own, in particular, a range of semiconductor stocks where we like the growth outlook. It is worth noting that part of the reason for Apple increasing the price of its latest phone is an increase in memory and components. This is a positive for semi-conductor stocks more generally, especially if a “feature war” breaks out in the smartphone space. We current hold a range of stocks that should be helped by this trend (Lam, Applied Materials, Skyworks, and to a lesser extent Cisco).

Click below the monthly performance heatmap:

In summary, our view continues to be that Australian investors are better off holding international investments at this point in the cycle. The past four months have obviously taken a big step in this direction, with international stocks providing almost 15% in just four months. While structurally we see this rising, it is unlikely to move in a straight line .

Our intention is that our portfolio is positioned to take advantage of our key themes but minimise risk in the event that our themes take longer than expected to resolve themselves.

We usually find that big picture macro themes take a long time to resolve themselves in financial markets, but when macro theme resolve themselves they do so quickly – usually too quickly to reposition your portfolio if you are not already invested.

Register your interest now (if you haven't already):

Damien Klassen is Head of Investments at Nucleus Wealth.

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen is an authorised representative of Nucleus Wealth Management, a Corporate Authorised Representative of Integrity Private Wealth Pty Ltd, AFSL 436298.

{kind=link}