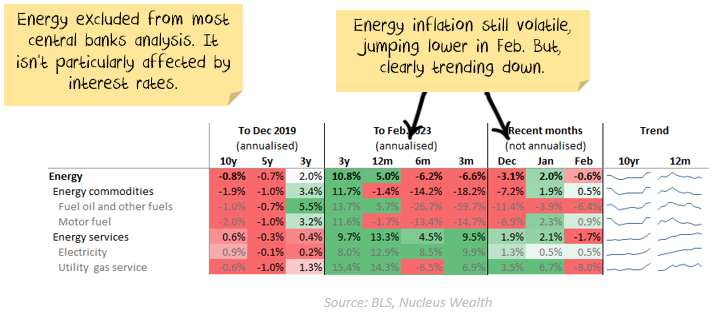

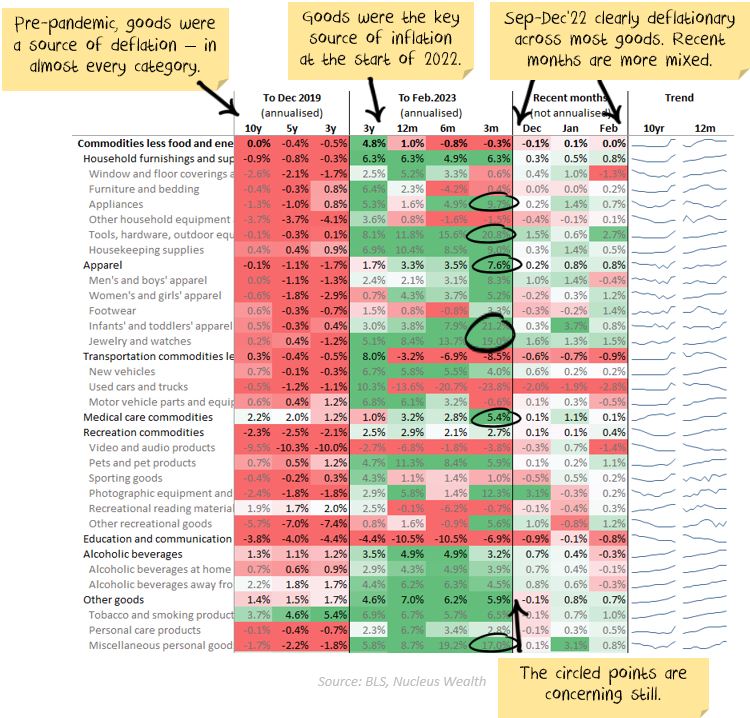

US inflation came in around expectations. More than a few data points in this report are reversing the recent trend of falling inflation. Based on surveys and upstream data points, I believe inflation is heading for deflation. But, this report did little to support the argument. See tables:

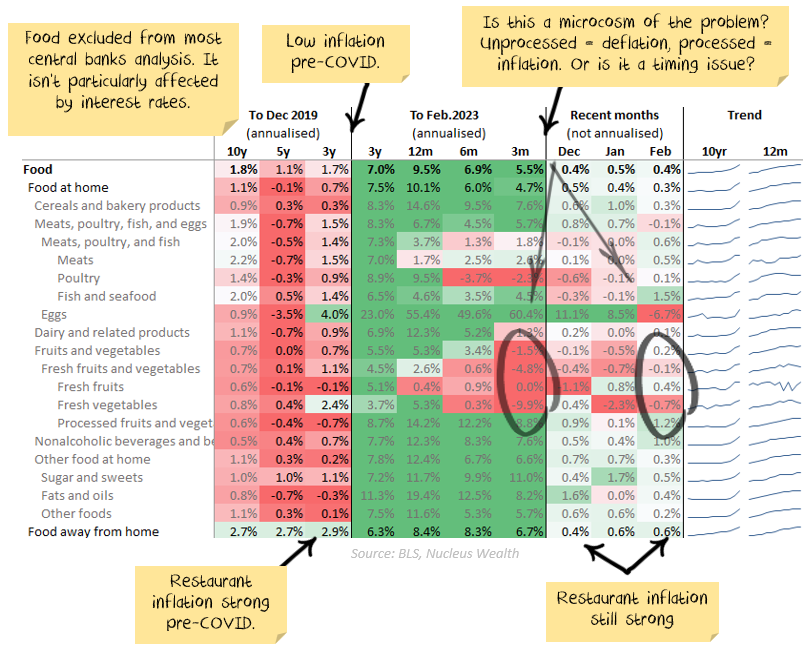

Fruit and vegetables are an example of a broader issue. Inflation ran hot in this category during 2022 but turned clearly deflationary in recent months. However, processed food and vegetables are still seeing rampant inflation, up 14.2% over the year, running at almost 9%p.a. over the last three months:

A few possible explanations:

Now each one of these arguments has some truth to it. Different sectors will have different characteristics, which will make one or other of the arguments stronger.

In the food category, with pretty low barriers to entry, I would expect timing and opportunity to play the largest part. In sectors with less competition, price falls become less likely.

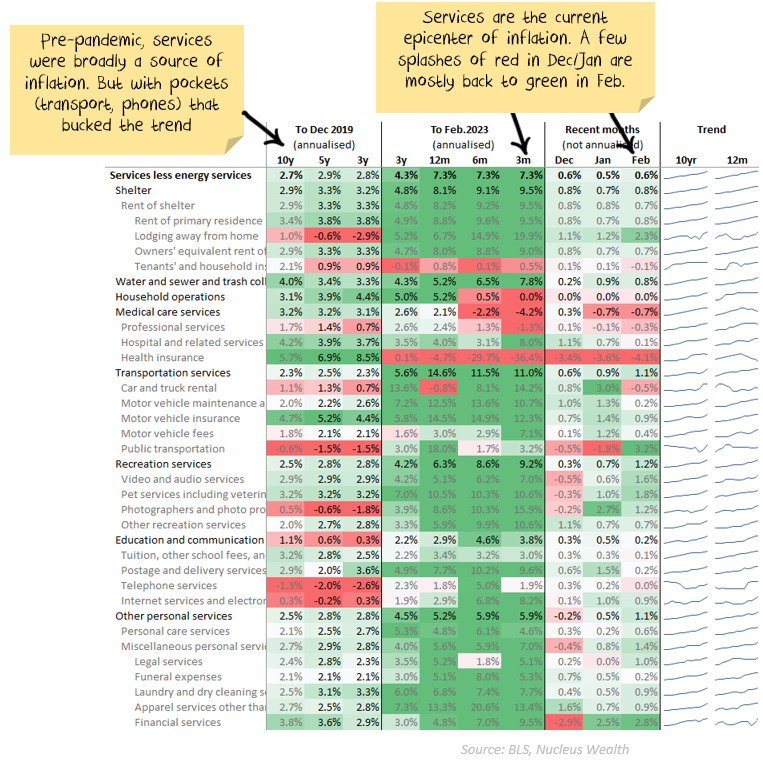

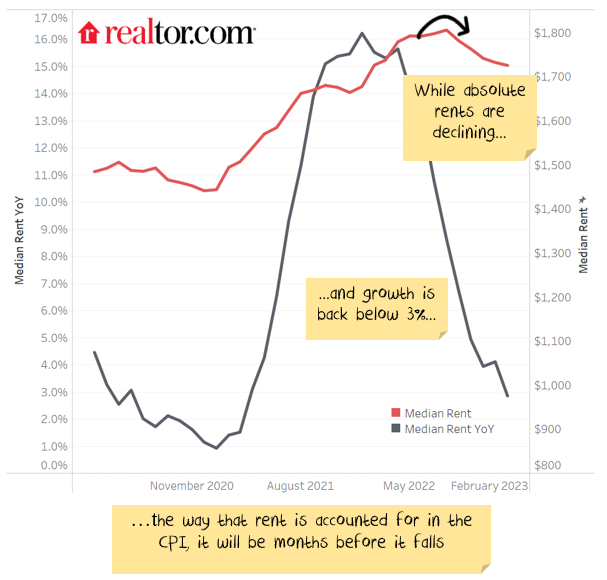

Rental inflation, the largest part of services inflation, is still running hot in the report. This is at odds with what participants are reporting:

It is a factor of how rents are calculated in the inflation numbers, reflecting that rental contracts don't all expire each month and so increase gradually.

The way the maths are at the moment, annual inflation is going to start falling rapidly over the coming months:

My expectation is that:

This report doesn't preclude a continued fall in inflation, but it doesn't support it either.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}